Why donation acceptance rates vary between payment providers (and why they matter)

Updated May 26, 2026

Between 5% and 10% of online donations fail behind the scenes, and not because of bad cards.

Payments, as TSG Payments put it, isn't a "big move" industry, it's a "game of inches." The difference in online donation acceptance rates between providers can run as wide as 13 percentage points, and it comes down to specific technical choices that decide whether a donor's gift reaches the cause.

Over the course of a year, those inches add up to big gains (or big losses).

Somewhere between 5% and 10% of online donations fail.

Not necessarily because a donor’s card is maxed out or expired, but because behind the scenes, the party processing the payment has dropped the ball in ways a donor will never see.

As TSG Payments recently put it in their 2026 Annual Report, “Payments isn’t a ‘big move’ industry. It’s an industry of basis points. It’s a game of inches.”

TSG’s comparison to sports is an apt one (to say nothing of the callback to Al Pacino’s epic speech in Any Given Sunday). Indeed, the journey a payment takes from the moment a donor clicks “submit” to the moment their gift is confirmed is a lot like marching up a football field; it’s a series of small, intentional steps with each one an opportunity to gain ground or lose it. Likewise, football’s a game of strategy and play-calling, and of knowing which routes to run and when to audible at the line.

This is the game of inches, and understanding why online donation acceptance rates vary between payment providers requires understanding what happens during those steps and which processors are calling the right plays.

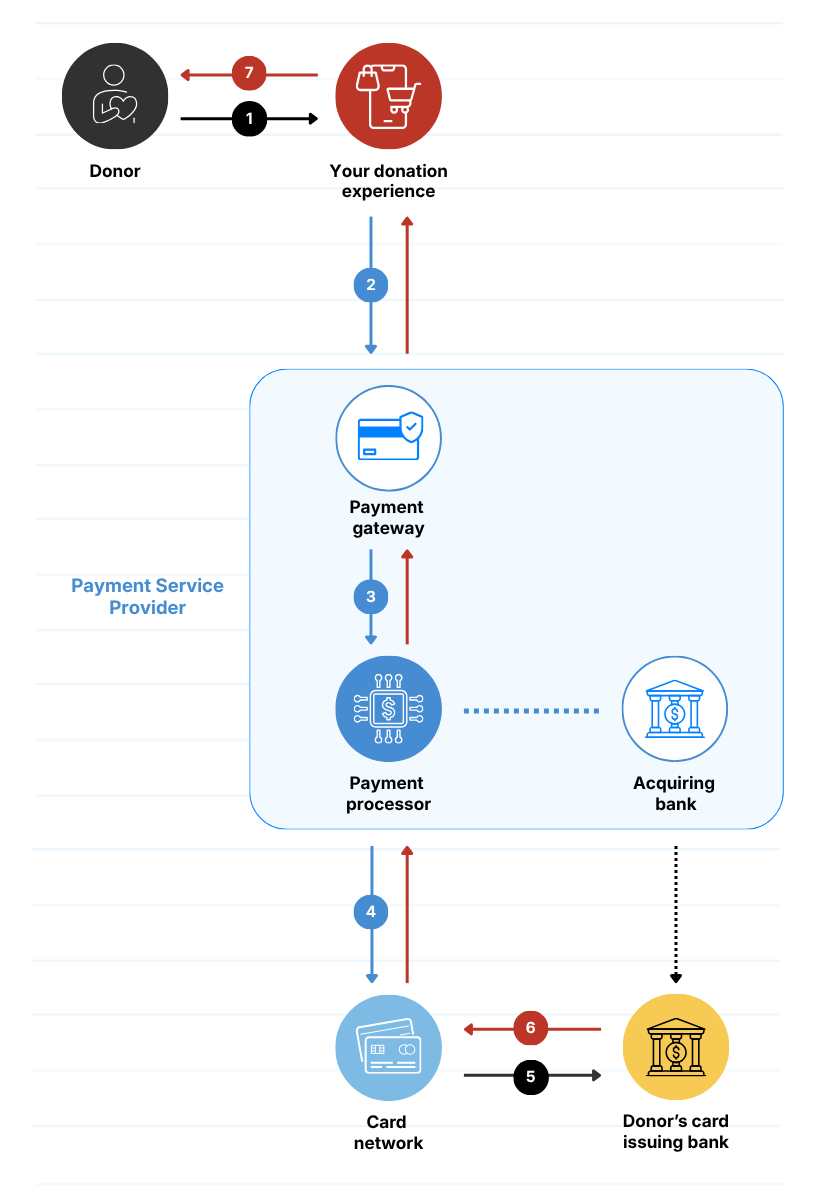

The Lifecycle of an Online Payment

To the donor, an online gift feels instantaneous. They enter their card number, click submit, and either see a confirmation or an error message.

Leading up to this result, though, there’s a multi-party relay race taking place behind the scenes, often in less than two seconds.

It works something like this:

- The process begins when the donor submits their payment information on a website

- The website the donor’s on captures that information and (hopefully securely) transmits that through the provider’s payment gateway (i.e. the merchant’s payment gateway)

- The payment gateway packages that data and sends it to the acquiring bank via a processor, which is the financial institution that processes payments on behalf of the organization.

- An acquirer then routes the transaction to the appropriate card network, whether that is Visa, Mastercard, American Express or another scheme.

- The card network forwards the request to the issuing bank, which is the bank that issued the donor’s card.

- The issuing bank must then make a decision in milliseconds, evaluating whether the card is valid, whether the account is in good standing, whether sufficient funds or credit are available, and whether the transaction appears legitimate based on fraud models, velocity checks, and behavioural analytics.

- If the issuing bank approves the transaction, an authorization code travels back through the same chain to the merchant, and the donor sees their confirmation (accepted). If the issuing bank declines, the donor sees an error (declined).

This four-party model, as described by JP Morgan’s payments documentation, places the card network at the centre, connecting the cardholder, the issuer, the acquirer, and the merchant. Every handoff between these players represents a potential point of failure, and the integrity of the data that moves through this chain directly influences whether the issuing bank feels confident enough to approve the transaction.

Why Acceptance Rates Differ: The Technical Realities

If every payment processor were simply passing the same data through the same pipes, then online donation acceptance rates – that is, the percentage of donations that processed successfully – would be roughly equivalent across the industry. They are not.

Benchmarks cited by payment orchestration platform GR4VY show acceptance rates ranging from above 90% in mature markets to as low as 50-70% in emerging ones, and even within the same market, the gap between a well-optimized processor and a legacy provider can be several percentage points.

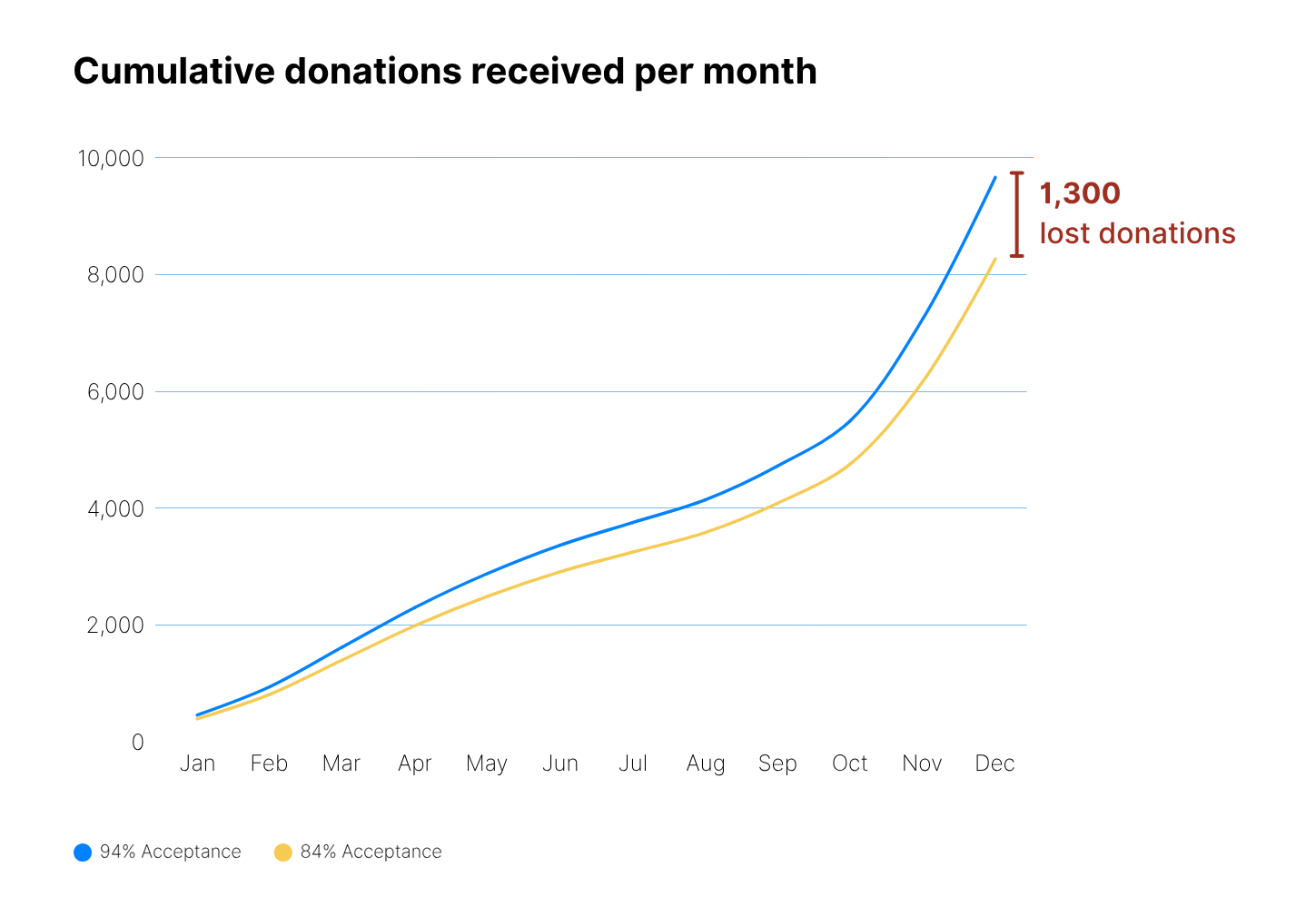

Our own data shows payment acceptance rates amongst providers range anywhere from 97% to as low as 84% for some providers.

At scale, those percentage points represent significant revenue, and for nonprofits, they represent donations that either reach your mission or vanish into the void of failed transactions.

The reasons for this variance are technical, but they are certainly not mysterious.

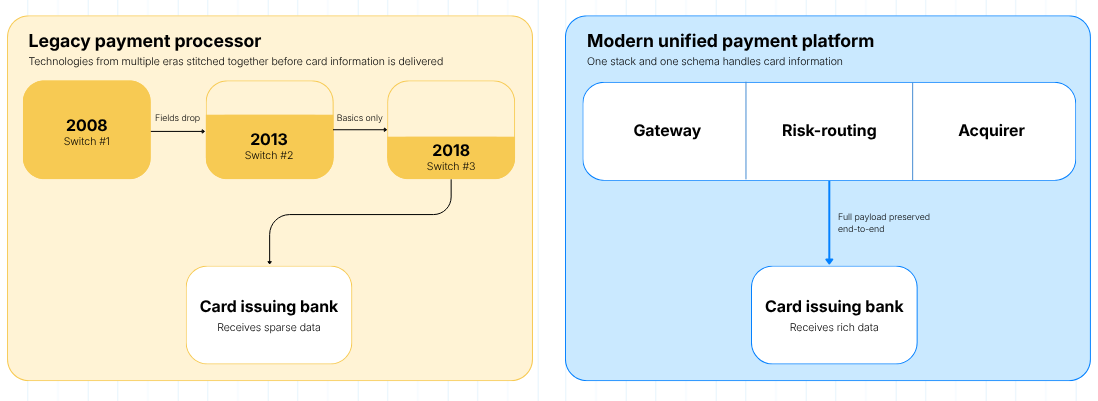

The Problem of Fragmented Architecture

Many of the largest payment providers in the market today aren’t single companies so much as they are collections of acquisitions stitched together over decades. Many processors have grown through mergers, and the result is that a transaction processed through their system passed through different internal “switches” before it ever reaches the issuing bank. Each of these switches was built by a different team, on different technology stacks with different security standards, and as a result, the data that enters one system does not always emerge from the other side intact.

This phenomenon is sometimes called “data degradation,” and it refers to the loss or simplification of cardholder data as it moves through multiple legacy layers. When the issuing bank receives a transaction request with sparse or generic data, it has less information to work with when making its approval decision, and less information often translates to a higher likelihood of decline.

Going back to our football analogy, think of these switches as more players getting involved in the game as a payment journeys downfield. Every time another player touches the bal, it gets a little muddier and more likely to be fumbled.

Modern processors that were built from the ground up on a single platform don’t have this problem. When the gateway, risk management, and acquiring functions all live within one system, the data that the donor entered at checkout arrives at the issuing bank in the same form with the same level of detail.

The difference may sound abstract, but becomes measurable in acceptance rates. According to a report from Checkout.com, up to 70% of IT budgets at financial institutions are spent maintaining outdated systems, and if left unchecked, these legacy platforms could cost the industry $57 billion by 2028. That’s a lot of lost transactions.

The Role of Data Richness

Issuing banks do not approve or decline transactions arbitrarily. They use fraud models, risk scoring, and pattern recognition to evaluate each request, and the more data they have to work with, the more confident they can be in their decision. A muddy transaction that arrives with only a card number and an amount looks riskier than one that arrives with device fingerprinting, a verified billing address, an IP address, an email, and authentication data from “3D Secure” protocols.

The difference between older and newer authentication protocols illustrates this clearly. The original 3D Secure protocol transferred roughly ten data points to the issuing bank. The updated 3DS2 protocol, per to EBANX, transfers over 100 data points. That tenfold increase in information gives the issuing bank substantially more context for evaluating whether a transaction is legitimate.

Legacy processors, often running on infrastructure that predates these protocols, tend to send what one industry comparison describes as “clean but sparse” data. It is technically valid, but it does not give the issuing bank much to work with. This can lead to things like false declines, fraud or both. Modern processors, by contrast, send enriched data that includes authentication details, network tokens, and behavioural signals that help the issuer feel comfortable approving the transaction.

According to Solidgate’s 2026 authorization rate optimization research, simply ensuring that the IP address field is populated drives an average acceptance rate increase of 0.35%, and including a validated customer email generates an additional 0.26%. These gains sound marginal in isolation, but applied to enterprise transaction volumes, they translate into meaningful recovered revenue. Visa has recognized this dynamic and is launching the Digital Commerce Authentication Program in April 2026, which will offer fee reductions to merchants who provide specific data elements like Device ID, IP address, email, and billing address.

Direct Acquiring vs. Multiple Intermediaries

The structure of the relationship between a payment processor and the card networks also matters. Some modern processors, like Adyen, hold their own banking licenses and function as both the processor and the acquiring bank. This means they own the full relationship with the card schemes and do not need to route transactions through additional intermediaries.

The advantage of this arrangement is both speed and transparency.

When a processor owns the acquiring relationship, they have better insight into why a particular issuing bank might decline a transaction, and they can optimize in real time with AI based on that feedback. When a processor is passing transactions through a third-party acquirer, on the other hand, that feedback loop is slower and less complete, and the opportunity to recover a failed transaction diminishes.

Intelligent Retry Logic vs. Lost Donations

Not every declined transaction is permanently lost. Surprising, right? The payments industry distinguishes between hard declines, which are permanent rejections for reasons like a stolen card or a closed account, and soft declines, which are temporary failures that can sometimes be resolved. Soft declines might result from insufficient funds, processor timeouts or overly sensitive fraud filters, and with the right approach, many of them can be recovered.

Legacy processors typically treat a decline as the end of the story. The transaction failed, and the donation is lost. Modern processors with intelligent retry logic take a different approach, automatically re-attempting failed payments with modified parameters in milliseconds. For example, a transaction that failed as a cross-border payment might succeed if retried with local routing. A transaction that timed out might succeed if retried a few seconds later.

According to Adyen, their “Auto Rescue” feature, which uses machine learning to selectively retry declined transactions when the failure is likely temporary, can boost recovery rates as high as 10%. Pinterest, for example, reported a 4% improvement in recovery rate on retried transactions during their pilot testing. For recurring giving programs, Adyen’s integration with card network billing updaters refreshes stored credentials in real-time, increasing card-on-file approval rates by approximately 2.5%.

Network Tokenization

One additional factor that influences acceptance rates is whether a processor uses network tokenization, which replaces static card numbers with dynamic tokens that update automatically when a donor’s card information changes. According to data cited by Solidgate, Visa reports that tokenization lifts authorization rates by approximately 4.7% while reducing e-commerce fraud by roughly one-third. Across Solidgate’s own merchant base, network tokenization improves acceptance rates by up to 15% on tokenized versus non-tokenized transactions from the same card cohort.

The benefit is particularly relevant for recurring giving programs, where a donor’s card might expire or be reissued between gifts. Without tokenization, the next scheduled donation would fail because the card on file is no longer valid. With network tokenization, the token updates automatically, and the donation processes successfully without the donor needing to take any action.

The Impact on Donor Experience

The technical details of payment processing don’t really matter to a donor, except when the experience fails them.

When a donation fails, the donor does not see a payment processor – let alone its fragmented architecture or the sparse data or the lack of retry logic behind the scenes – they see an error message, and that error message creates friction.

Some folks will try again with a different card, many will not.

They might assume the organization’s website is broken, they may simply move on with their day and forget to return – or worse, they may decide that because of the experience, they don’t trust the work the cause does.

Indeed, the intent to give was there, but the infrastructure failed them and the organization never receives the gift.

In this way, TSG’s observation that payments is an industry of basis points is ultimately a statement about how success in this space compounds. A processor that achieves a 2% higher acceptance rate than a competitor is reaching the donors who would have walked away, and over the course of a year, across thousands of donations, those 2% of recovered gifts add up to a material difference in funds raised.

Adding Up the Inches

The variance in acceptance rates between payment providers is not random, nor is it simply a matter of one provider being “better” than another in some vague sense.

It’s the result of specific technical choices: whether the processor operates on a single platform or a patchwork of acquisitions, whether they send enriched data or sparse data to issuing banks, whether they hold direct acquiring relationships or route through intermediaries, whether they offer local acquiring globally or fragment by region, whether they employ intelligent retry logic or treat declines as final, and whether they use network tokenization to keep card credentials current.

Each of these factors contributes a few inches, and when you stack them all together, the gap between a legacy payment provider and a modern one becomes significant. For organizations that depend on generosity to fund their work, understanding this game of inches is as much an operational concern as it is a strategic one.

What your journey are your online donations on? Reach out to chat payments with us any time.